The Origins of the “Sell in May” Strategy

The phrase “Sell in May and go away” is believed to have originated in 17th-century England, when wealthy investors would leave London for the summer. This led to a seasonal drop in trading activity and weaker stock market performance. Over time, this pattern gave rise to the notion that exiting the market in May and returning in the fall could boost returns.

Does the Strategy Hold Up in the Data?

We compared two S&P 500 investment strategies using data from 1990 to 2024:

May–October: Invest each year from May 1 to October 31

November–April: Invest from November 1 to April 30

Returns were calculated using the index levels at the beginning and end of each period, compounded annually.

The results show that the November–April period consistently outperformed the May–October window, aligning with the seasonal strength typically seen in fall and winter.

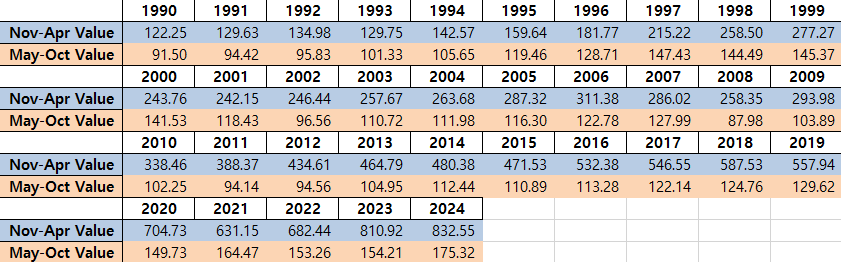

2001–2011: “Sell in May” Was Effective

Between 2001 and 2011, May–October returns were often negative and volatile:

Notable drops in 2001 (-16.3%), 2002 (-18.5%), 2007 (-31.3%), and 2008 (-7.9%)

Average return for the period: -2.5%

During this period, “Sell in May” appeared to work as intended.

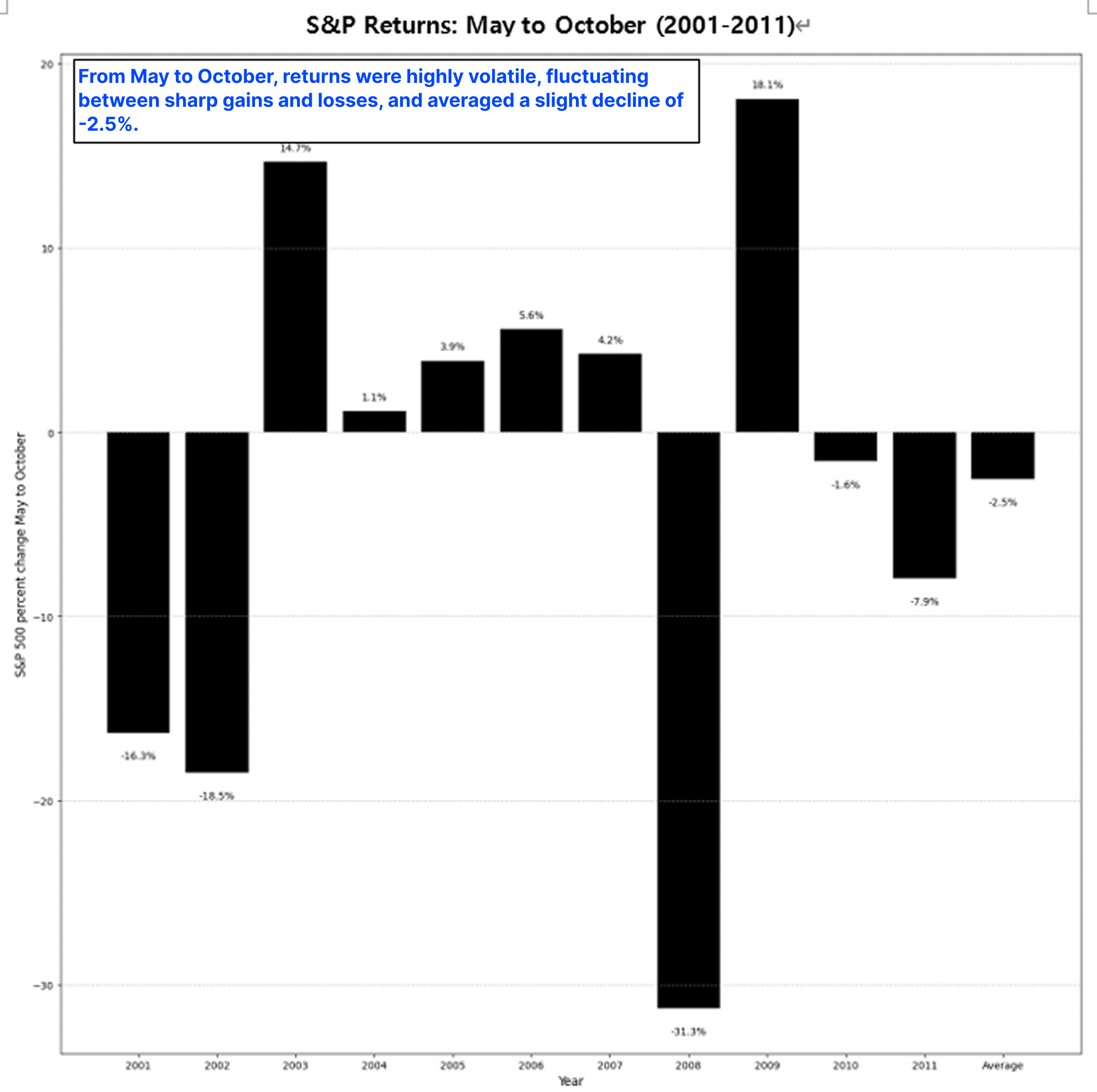

2012–2024: Seasonal Weakness Fades

The trend changed in the last decade:

Strong gains in 2012 (11.0%), 2017 (7.8%), 2019 (15.5%), 2020 (13.7%), and 2024 (13.7%)

Fewer and less severe summer declines

Average return for May–October: +5.1%

These results suggest the seasonal pattern has weakened significantly.

Why the Shift?

Several factors likely contributed:

Increased global capital mobility

Advances in technology and year-round trading activity

Broader investor participation, including institutions and retail investors

These shifts have made markets more resilient across all seasons, reducing the impact of traditional seasonal biases.

Conclusion

While the “Sell in May” strategy once had merit, recent market behavior shows that seasonal investing is far less effective today. Instead of relying on outdated calendar rules, investors should build strategies based on fundamentals, macroeconomic conditions, and data-driven analysis.

[Compliance Note]

All posts by Sellsmart are for informational purposes only. Final investment decisions should be made with careful judgment and at the investor’s own risk.

The content of this post may be inaccurate, and any profits or losses resulting from trades are solely the responsibility of the investor.

Core16 may hold positions in the stocks mentioned in this post and may buy or sell them at any time.