n the stock market, there are always ample reasons to sell. When the “March stock market massacre” occurred, investors wondered whether they should sell because the market seemed likely to fall further. Now, however, as the market appears poised to continue rising both more significantly and more rapidly, many are confused about whether to sell.

Investors who sold stocks when the market was near its bear market lows a few months ago often suffer more with their positions than those currently contemplating a sale. Every time you need to make a major change in your asset allocation, the decision is difficult—especially as retirement approaches, when your human capital diminishes and you have less time to endure a painful bear market compared to younger investors.

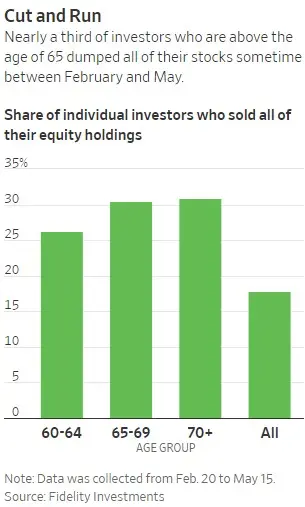

According to Fidelity and the Wall Street Journal, older investors tend to sell more during bear markets than younger ones. Fidelity’s data show that nearly one-third of investors aged 65 and above sold most of their holdings between February and May, and 18% of all customers completely liquidated their positions. I have discussed with many investors who wanted to sell in March; many were concerned about how prolonged downturns might affect their retirement plans. I fully understand why these retirees feel that their happiness is closely tied to their portfolios. The U.S. stock market enjoyed gains for 10 out of 11 years until 2020. This crisis was even likened to a second version of the Great Depression of the 1930s.

We are indeed living in frightening times.

However, fear and panic are not sufficient or valid reasons to sell. Waiting to sell until the market stabilizes can be a disastrous strategy. Even valuation-based market timing indicators have become almost useless—something anyone who has traded based on fundamentals over the past 20–30 years can attest to.

A bear market is one of the worst times to completely overturn your asset allocation, because your decision-making ability is often clouded by emotion.

So, when should you sell all or part of your stock holdings?

When It’s Time for Rebalancing

Going all in or completely exiting your position are among the riskiest moves in investing. While you might occasionally be influenced by luck, in reality you tend to sell before a major bull market begins or buy before a significant bear market sets in. Unless you have a rules-based investment strategy that you can stick to for a lifetime, extreme strategies like these are prone to leading to huge mistakes at the worst possible time.

The simplest sell strategy is to adjust your portfolio allocation according to predetermined targets or timelines. For example, after the stock market rose by more than 30% in 2019, some investors sold part of their stock holdings to purchase bonds, cash, or other investments—only to see the stock market surge afterward. Then, after the market fell by over 30% this spring and bonds played a key role in a balanced portfolio, they sold bonds to buy more stocks. Today, those stocks are up 40%—a truly remarkable decision.When Diversification Is Needed

I have seen many investors who allocated most of their retirement assets to the stock market instead of bonds. This strategy isn’t for the faint of heart—it works for pure savers who can endure short-term financial pain.

When your investment period ends and retirement forces you to start drawing down your assets, a new dynamic comes into play. No one wants to be forced to sell stocks in a depressed bear market just to meet expenses. Even the most risk-tolerant investors eventually feel the need to cover expenses with cash or bonds.

A severe bear market might not be the ideal time to seize an investment opportunity, but a significant bull market is never a bad time to re-evaluate your diversified portfolio.When You Realize You’ve Misunderstood the Investment Theme

This is particularly relevant for those holding concentrated positions in individual stocks or niche ETFs. Every investor should regularly check whether their entry and exit points for an unexplained investment idea are still valid.

This is more difficult than it seems. Questions like, “What if I wait until I just break even?” or “What if I sell and it immediately soars?” are common pitfalls that can be seen in losing positions.When You’ve Won Big in the Game

If you’ve been fortunate enough to accumulate an enormous sum—say, 20 to 25 times your expected retirement expenses—and have managed your spending habits well, you might eventually ask yourself, “What’s the point of continuing to take risks?”

In a world where risk-free returns are available, such decisions would be trivial. However, the environment where you can simply live off interest from high-quality bonds no longer exists.

Yet, if you have sufficient surplus funds to defend against inflation for the rest of your life, you might find that it becomes increasingly difficult to bear the myriad market risks in your portfolio.When You Need to Reassess Your Risk Profile or Adjust for a Change in Investment Period or Environment

Most investors believe that portfolio changes should be driven solely by market characteristics. Consider factors like the CAPE ratio, interest rates, Tobin’s Q formula, the A/D line, investor sentiment, and short-, medium-, and long-term performance metrics.

Understanding the past and present market conditions can help guide your future decisions, though not every portfolio decision needs to be based solely on market fundamentals.

Additionally, consider how your current environment affects your risk tolerance. You might need to reduce risk exposure if you find yourself in a better situation than expected—perhaps you’ve received an unexpected windfall or spent less than anticipated.

If you don’t have a clear understanding of your investment goals from the start, building a portfolio becomes nearly impossible.

While the market is critically important, you must always base your decisions on your own environment and goals.

<Source: awealthofcommonsense>