I’ve been thinking a lot about if this could be the end…

On the Morning Show today we talked about whether the bull market for stocks could continue if we lost Bitcoin.

The answer is it definitely could. But, wouldn’t it be strange?

Crypto and stocks have danced together for a long time.

However, I think it’s less about crypto and more about the overall risk appetite of the market.

Bitcoin is just one part of it. When I think about risk on corners of the market and the kind of things that should be working during a healthy bull cycle I’m thinking of homebuilders, semiconductors, and banks… to name a few groups.

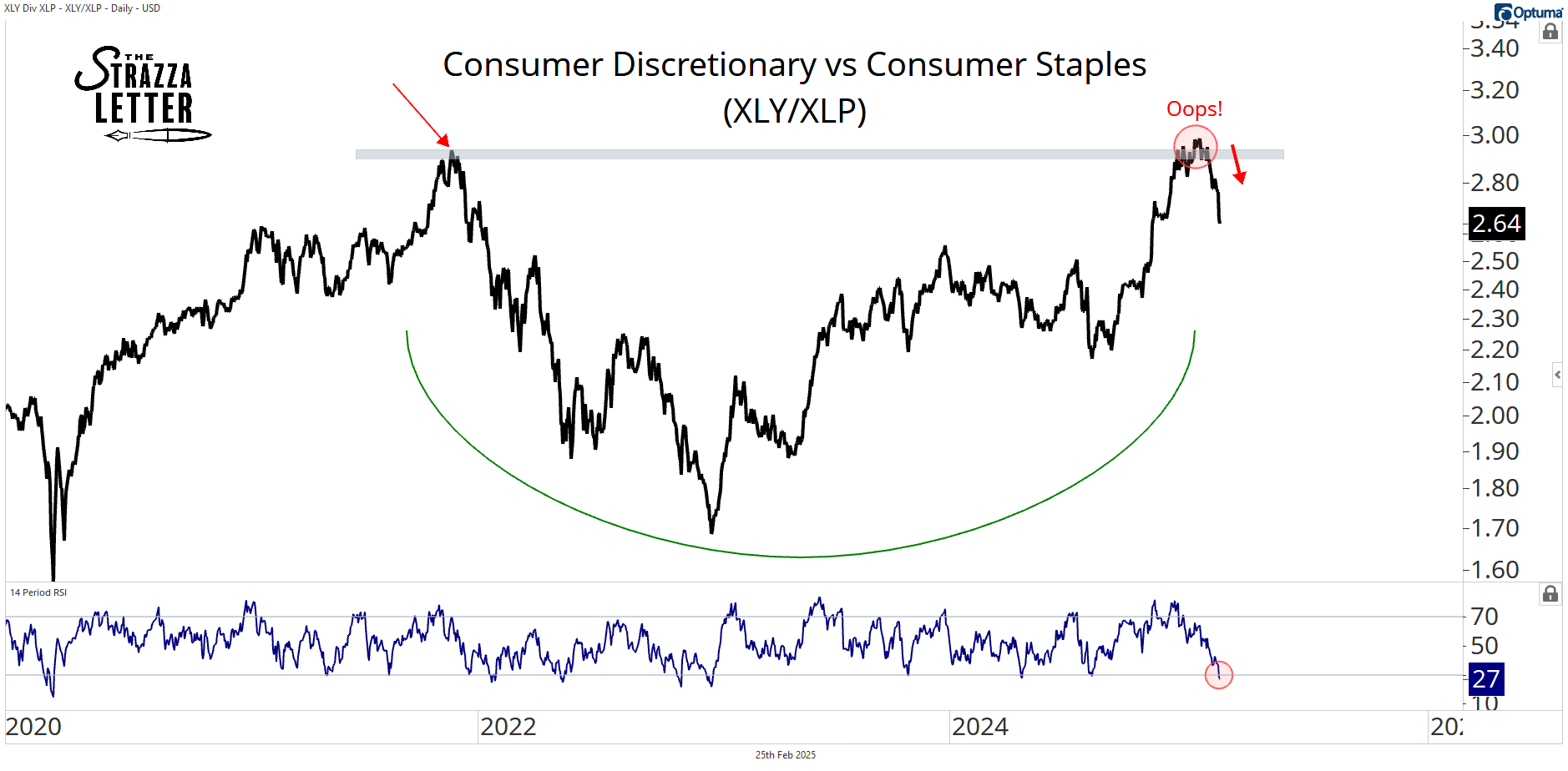

But I’m also looking into the relationships between groups. In particular, I’m analyzing the performance of offensive stocks versus defensive stocks. The best ratio for this has always been discretionary vs staples.

XLY/XLP ranks second to none when it comes to the assessment of risk appetite.

Are investors buying the risky consumer stocks and betting on growth?

Or are they favoring the defensive ones and playing it safe?

As a bull, you always want new highs in the stock market to be confirmed by the discretionary vs staples ratio. Right now, not only is XLY/XLP not supporting new highs, but it is flashing a dire warning sign.

XLY/XLP just printed a nasty failed breakout and sold off to fresh multi-month lows. The ratio has now given back all of its post-election gains and violated its VWAP from the August low.

The tactical trend has turned down, and the primary trend is in jeopardy. Momentum just hit its most oversold reading since the bear market lows in 2022.

A valid breakdown in this relationship would mean further leadership from defensive stocks in the future. Over any sustained timeframe, this would constitute bear market behavior.

I’m not saying it has to happen, but it’s where things are headed right now.

And while the discretionary vs staples ratio is only one data point, it’s a pretty damn bearish one.